|

WASHINGTON – As part of a larger effort to protect small businesses and organizations from scams, the Internal Revenue Service today announced the details of a special withdrawal process to help those who filed an Employee Retention Credit (ERC) claim and are concerned about its accuracy.

This new withdrawal option allows certain employers that filed an ERC claim but have not yet received a refund to withdraw their submission and avoid future repayment, interest and penalties. Employers that submitted an ERC claim that’s still being processed can withdraw their claim and avoid the possibility of getting a refund for which they’re ineligible. The IRS created the withdrawal option to help small business owners and others who were pressured or misled by ERC marketers or promoters into filing ineligible claims. Claims that are withdrawn will be treated as if they were never filed. The IRS will not impose penalties or interest. Those who willfully filed a fraudulent claim, or those who assisted or conspired in such conduct, should be aware that withdrawing a fraudulent claim will not exempt them from potential criminal investigation and prosecution. “The IRS is committed to helping small businesses and others caught up in this onslaught of Employee Retention Credit marketing,” said IRS Commissioner Danny Werfel. “The aggressive marketing of these schemes has harmed well-meaning businesses and organizations, and some are having second thoughts about their claims. We want to give these taxpayers a way out. The withdrawal option allows employers with pending claims to avoid future problems, and we encourage them to closely review the withdrawal option and the requirements. We continue to urge taxpayers to consult with a trusted tax professional rather than a marketing company about this complex tax credit.” When properly claimed, the ERC – also referred to as the Employee Retention Tax Credit or ERTC – is a refundable tax credit designed for businesses that continued paying employees during the COVID-19 pandemic while their business operations were fully or partially suspended due to a government order, or they had a significant decline in gross receipts during the eligibility periods. The credit is not available to individuals. The ERC is a complex credit with precise requirements to help businesses during the pandemic, and since mid-September, the IRS has received approximately 3.6 million claims for the credit over the course of the program. In July, the IRS said it was shifting its focus to review ERC claims for compliance concerns, including intensifying audit work and criminal investigations on promoters and businesses filing dubious claims. The IRS has hundreds of criminal cases being worked, and thousands of ERC claims have been referred for audit. The new withdrawal process follows the Sept. 14 announcement of an immediate moratorium on processing new ERC claims. The moratorium, which will last until at least the end of this year, follows a flood of ineligible ERC claims. Payouts for claims submitted before Sept. 14 will continue during the moratorium period but at a slower pace due to more detailed compliance reviews. With stricter compliance reviews in place, existing ERC claims will go from a standard processing goal of 90 days to 180 days – and much longer if the claim faces further review or audit. The IRS may also seek additional documentation from the taxpayer to ensure the claim is legitimate. Enhanced compliance reviews of existing claims submitted before the moratorium is critical to protect against fraud but also to protect businesses and organizations from facing penalties or interest payments stemming from bad claims pushed by promoters. The IRS continues to warn taxpayers to use extreme caution before applying for the ERC as aggressive maneuvers continue by marketers and scammers. The IRS is also working on guidance to help employers that were misled into claiming the ERC and have already received the payment. More details will be available this fall. Who can ask to withdraw an ERC claim Employers can use the ERC claim withdrawal process if all of the following apply: They made the claim on an adjusted employment return (Forms 941-X, 943-X, 944-X, CT-1X). They filed the adjusted return only to claim the ERC, and they made no other adjustments. They want to withdraw the entire amount of their ERC claim. The IRS has not paid their claim, or the IRS has paid the claim, but they haven’t cashed or deposited the refund check. Taxpayers who are not eligible to use the withdrawal process can reduce or eliminate their ERC claim by filing an amended return. For details, see the Correcting an ERC claim – Amending a return section of the frequently asked questions about the ERC. How to withdraw an ERC claim To take advantage of the claim withdrawal procedure, taxpayers should carefully follow the special instructions at IRS.gov/withdrawmyERC, summarized below. Taxpayers whose professional payroll company filed their ERC claim should consult with the payroll company. The payroll company may need to submit the withdrawal request for the taxpayer, depending on whether the taxpayer’s ERC claim was filed individually or batched with others. Taxpayers who filed their ERC claims themselves, haven’t received, cashed or deposited a refund check and have not been notified their claim is under audit should fax withdrawal requests to the IRS using a computer or mobile device. The IRS has set up a special fax line to receive withdrawal requests. This enables the agency to stop processing before the refund is approved. Taxpayers who are unable to fax their withdrawal using a computer or mobile device can mail their request, but this will take longer for the IRS to receive. Employers who have been notified they are under audit can send the withdrawal request to the assigned examiner or respond to the audit notice if no examiner has been assigned. Those who received a refund check, but haven’t cashed or deposited it, can still withdraw their claim. They should mail the voided check with their withdrawal request using the instructions at IRS.gov/withdrawmyERC. Upcoming webinar and other resources for help Tax professionals and others can register for a Nov. 2 IRS webinar, Employee Retention Credit: Latest information on the moratorium and options for withdrawing or correcting previously filed claims. Those who can’t attend can view a recording later. The IRS unveiled a new question and answer checklist last month to help taxpayers understand if they’re eligible for the credit. Since then, the IRS evolved the checklist into an interactive IRS.gov feature to help employers – and the tax professionals working with them – check potential ERC eligibility. The IRS also continues to encourage employers to seek out a trusted tax professional who understands the complex ERC rules, not a promoter or marketer trying to get a hefty contingency fee while taking advantage of honest taxpayers. New approach from scammers Marketers and scammers have already revised their ERC pitches following the Sept. 14 moratorium announcement. Some are pushing employers who submit an ERC claim into agreeing to costly up-front loans in anticipation of a refund. The IRS urges taxpayers to avoid these loans and also learn the warning signs of ERC scams. "Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA

0 Comments

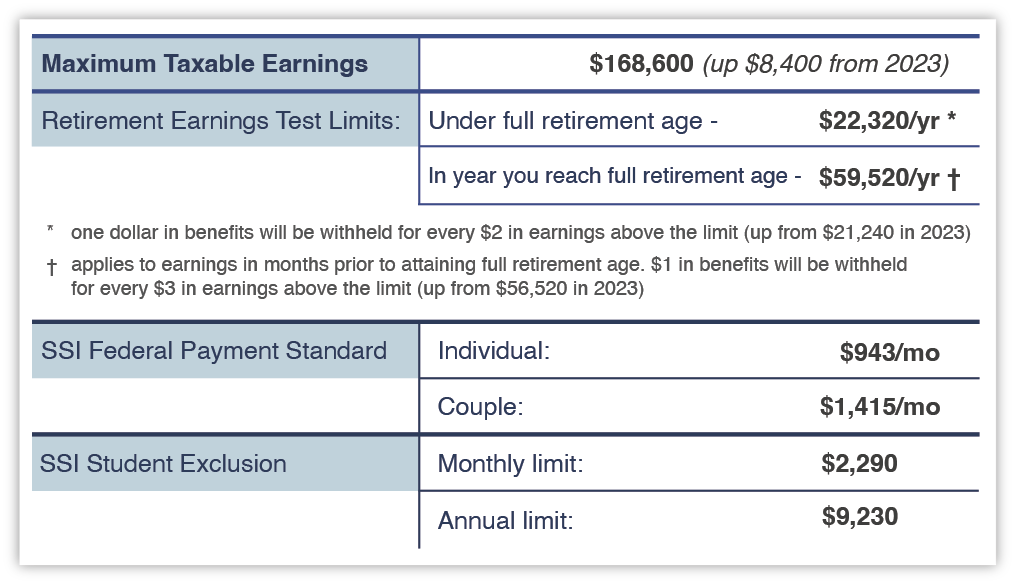

How much you pay and checks received are all going up! The Social Security Administration announced a 3.2% boost to monthly Social Security and Supplemental Security Income (SSI) benefits for 2024, a big drop from last year's increase of 8.7%. The increase is based on the rise in the Consumer Price Index over the past 12 months ending in September 2023. For those contributing to Social Security through wages, the potential maximum income subject to Social Security taxes is increasing to $168,600. This represents a 5% increase in your Social Security taxes! Here's a recap of the key dollar amounts:  2024 Social Security Benefits - Key Information

What it means for you

Social Security & Medicare Rates The Social Security and Medicare tax rates do not change from 2023 to 2024. The rates are 6.20 percent for Social Security and 1.45 percent for Medicare. There is also a 0.9 percent Medicare wages surtax for single taxpayers with wages above $200,000 ($250,000 for joint filers) that is not reflected in these figures. Please note that your employer also pays a 6.2 percent Social Security tax and a 1.45 percent Medicare tax on your behalf. These amounts are reflected in the self-employment tax rate of 15.3%, as self-employed individuals pay both halves of the tax rate. "Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA What every taxpayer should know You can begin receiving your Social Security retirement benefit as early as age 62. But by putting off your benefit start date you can receive a check that is approximately 8 percent higher for each year you delay receiving your benefit.

The basics Full retirement age. Those born between 1943 and 1954 reach their full Social Security benefit payment at age 66*. This is called your full retirement age. Early benefit penalty. Those same retirees can begin receiving their benefit at age 62. But if you start your benefits before reaching your full retirement age, the amount paid to you is permanently reduced. Bonus payment amounts. But there is also a bonus for each year you delay receiving benefits past your full retirement age. Your Social Security benefit is increased by 8 percent per year. The maximum cap amount. After age 70, the Social Security benefit is maximized. Further delay in starting your benefits adds no additional payments. Is a delay worth the wait? Here are reasons to delay receiving your Social Security benefits until you reach age 70: You expect to live longer. If your parents and grandparents lived long lives, you may wish to delay receipt of your initial Social Security benefits. The opposite is true if you have a shorter life expectancy. You do not need the income. If you are still working or have alternative income sources, it may be better to delay receiving your benefits. An 8 percent increase in monthly payments is a good increase versus other investment alternatives. Your spouse has died. You will need to review the possibility of receiving survivor benefits based on your spouse’s earnings. Later, you could then start collecting your own Social Security retirement benefits based on your earnings. Your benefits are taxed. If you have other income, your Social Security retirement benefits could be subject to income tax if you are not yet at the full retirement age. Should you delay receiving your Social Security benefits? There often is not one answer that fits all situations. Consider reviewing your situation prior to making a decision. * Full retirement age increases by two months each year after 1954 until reaching full retirement age of 67 for those born in 1960 or later. "Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA  While most income received from your employer quickly ends up on a W-2 tax form at the end of the year, here are some common employee benefits that often avoid the impact of Federal taxes.

Health benefits. While now reported on W-2's, employer provided health insurance premiums are currently not required to be reported as additional income by the employee. This includes premiums paid for the employee and qualified family members. In addition, the employee portion of premiums can be paid in pre-tax dollars. Credit card airline miles. Credit card benefits like miles are not generally deemed as taxable income. So those miles earned on corporate credit cards that go to you as an individual are not likely to increase your tax bill. Employee tuition reimbursement. Up to $5,250 of tuition reimbursed to you by your employer are not deemed to be additional taxable income. Commuting expenses. You can generally exclude the value of transportation benefits you receive up to $300 per month for combined commuter highway vehicle transportation and transit passes. There is also up to $300 per month for tax-free qualified parking benefits. Company Health Savings Account (HSA) contributions. Up to specified dollar limits, cash contributions to the HSA of a qualified individual are exempt from federal income tax withholding, social security tax, Medicare tax, and FUTA tax. Group term life insurance. You can generally exclude the cost of up to $50,000 of group-term life insurance from your wages. Small gifts. Small-valued gifts are not included in income and could include things like the use of the company copy machine, occasional meals, reasonably priced holiday gifts and tickets to a sporting event. Knowing what benefits can avoid a tax bite, try to maximize their use to your greatest advantage and reach out with any questions you may have. "Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA When disaster strikes, Americans can always be counted on to help. That help comes in countless ways, but often the easiest way to help is by donating money to charities.

Sadly, criminals are just as likely to answer the call after a disaster or emergency as the millions of people who open their wallets. Scammers solicit donations to fake charities and can pose as employees of legitimate charities or federal agencies to dupe disaster victims trying to get disaster relief. Although some legitimate charities do contact people out of the blue, people should always be suspicious of unsolicited contact. Taxpayers donating money should keep a few things in mind: Use the IRS Tax Exempt Organization Search tool to find or verify qualified charities. Donations to these real charities may be tax deductible. Research a charity before sending a donation to confirm that the charity is real and to know whether the donation is tax deductible. Always get a receipt and keep a record of the donation. Review bank and credit card statements closely to make sure donation amounts are accurate. Keep scammers’ tricks in mind: Legitimate charities do not ask for gift cards, cash, or wire transfers. Scammers may claim to work for the IRS or another government agency. Thieves may pose as a representative of a legitimate charity to ask for money or private information from well-intentioned taxpayers. Scammers can change their caller ID to make it appear they are a legitimate organization calling from a legitimate phone number. Scammers make vague and sentimental claims but give no specifics about how your donation will be used. Scammers set up bogus websites using names that sound like real charities. Bogus organizations often claim a donation is tax deductible when it’s not. Disaster victims should know: Disaster victims can call the IRS disaster assistance line at 866-562-5227. IRS representatives will answer questions about tax relief or disaster-related tax issues. Donating to a charity is a great way to help others after a disaster or emergency. If taxpayers suspect a scam or fraud, they can report it to The Federal Trade Commission. More Information: National Center for Disaster Fraud DisasterAssistance.gov Publication 3067, IRS Disaster Assistance – Federally Declared Disaster Area "Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA Now is the time to make your estimated tax payment If you have not already done so, now is the time to review your tax situation and make an estimated quarterly tax payment using Form 1040-ES. The third quarter due date is now here.

Due date: Friday, Sept. 15, 2023 You are required to withhold at least 90 percent of your 2023 tax obligation or 100 percent of your 2022 obligation.* A quick look at last year’s tax return and a projection of this year’s obligation can help determine if a payment is necessary. Here are some other things to consider:

*If your income is more than $150,000 ($75,000 if married filing separately), you must pay 110 percent of your 2022 tax obligation to be safe from an underpayment penalty. "Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA Not all income is the same in the eyes of the tax code The tax code uses jargon that can be confusing for the unwary. One of them that impacts most of us is the term unearned income. Unearned income is often defined as anything that is not earned income. If you find this kind of definition a little too vague, here is some clarity.

Tax code definition Before providing the definition of unearned income, take a quick look at what is typically included in both earned and unearned income. Earned income includes salaries, wages, tips, professional fees, and taxable scholarship and fellowship grants. Employees will typically see this recorded in an annual W-2 tax form. Unearned income includes taxable interest, ordinary dividends, and capital gain distributions. It also includes unemployment compensation, taxable social security benefits, pensions, annuities, and distributions of unearned income from a trust. Much of this income is often (but not always) recorded using 1099 tax forms. Why does it matter? If the tax code was simple, it wouldn't matter one bit whether your income was earned income or unearned income. But this isn't the case. Here are some things to consider: Different tax rates. While most earned income is subject to ordinary income tax rates up to 37%, unearned income can be subject to different tax rates. Long term capital gains and certain dividends, for instance, are generally subject to lower capital gains tax rates. These tax rates can max out at 20% before a potential net investment income tax of 3.8% is applied. Kiddie tax rules. The tax code limits the amount of unearned income that can be taxed at your dependent's (usually lower) income tax rate. Amounts over this limit are taxed at the parent’s rate. The amount is $2,500 in 2023. Tax benefit limits. Many tax credits and deductions will limit the amount of unearned income you may have and still qualify for a tax break. As an example, the Earned Income Tax Credit limits disqualified (unearned) income to $11,000 in 2023. Timing matters. Sometimes the timing of an event can shift unearned income from ordinary income tax rates to preferential gain tax rates. This is the case with investment sales. Hold an investment for one year or less before selling it and your unearned investment gain is taxed as ordinary income. Hold it longer than one year and the unearned income is taxed at capital gains tax rates. It's all in the details It's important to understand how all elements of income apply to different aspects of the tax code. This is where working with someone familiar with the code can help. "Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA Certain businesses that receive payments of over $10,000 in cash must file Form 8300, Report of Cash Payments Over $10,000 Received in a Trade or Business, electronically starting in 2024, the IRS said Wednesday in a news release (IR-2023-157). This new requirement applies to businesses that are required to file at least 10 information returns of one or more types other than Form 8300 in 2024.

Over 400,000 Forms 8300 were filed in calendar year 2022. An IRS representative said the Service was not immediately able to determine the number of Forms 8300 that were filed on paper versus electronically. The IRS noted that although many cash transactions are legitimate, the information on a Form 8300 can help the government fight tax evaders and drug traders, along with those who finance terrorism. Businesses can create an account with FinCen's BSA E-Filing System to e-file Forms 8300. A person generally must file Form 8300 within 15 days after the date the person received the cash. A business must keep a copy of every Form 8300 it files, along with any supporting documentation and the required statement it sends to customers, for five years from the date filed. Merely retaining the email confirmation of the filing of a Form 8300 does not meet the record-keeping requirement, the IRS said. Filers also must save a copy of the form — either electronically or on paper — before they finalize the submission and should associate the confirmation number they receive with the copy. A business may file a request for a waiver from electronically filing information returns, including Form 8300, because of undue hardship. However, a business may not request an e-filing waiver that would apply just to Form 8300. The business must include the word "Waiver" on the center top of each Form 8300 (page 1) when submitting a paper filed return. Also, filers are automatically exempt from filing Form 8300 electronically if using the required technology conflicts with their religious beliefs. The filer must include the words "RELIGIOUS EXEMPTION" on the center top of each Form 8300 (page 1) when submitting the paper filed return. The IRS issued a fact sheet, FS-2023-19, with details on the requirement. https://www.journalofaccountancy.com/news/2023/aug/businesses-must-e-file-form-8300-for-10000-cash-payments-2024.html "Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA  If you contribute too much money into your IRA during the year, how do you correct the problem without facing a tax penalty? Here are some tips.

Remember the annual limits 2023 Annual IRA contribution limits

What causes excess contributions Excess contributions can be caused by:

Corrective action and penalty If you place too much money into your retirement account you have until the tax filing deadline including any extensions to remove the excess contribution. Any excess amount will be subject to a 6% penalty for each year the excess contribution remains in your account. You may also owe tax on contributions and earnings created by the excess contribution. In addition: Traditional IRAs. You will need to account for the additional income on your tax return. So if you discover the problem after you file your income tax return, you may need to file an amended tax return. Roth IRAs. You can move excess contributions into the next year as long as IRA contributions in the following year are below the maximum allowed. Any earnings made during the time the excess contributions were in your account is taxable. Some ideas What can you do to minimize the risk of excess contributions? Make it automatic. Set up an automatic withdrawal from your checking account to fund your IRA. Conduct the math to ensure you will never contribute too much. Make a lump sum contribution. Make a one-time contribution at the beginning or end of each year. Want to wait for your refund? Remember you have until April 15th of the following year to fund your IRA. Consider taking advantage of this additional time. Rollovers are not contributions. Remember rollovers ARE NOT contributions so the annual contribution limits do not apply. If you wish to roll funds from a qualified plan into your IRA, the excess contribution limits will not impact you as long as the rollover is handled correctly. It is a good idea to seek expert help in this area to ensure your rollover is compliant with tax code. For instance, there are usually tax obligations if the rollover is from a traditional IRA into a Roth IRA. "Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA What to do if you miss a quarterly estimated tax payment Many clients like to keep their Federal Tax withholdings as low as possible to avoid the IRS having their funds interest-free throughout the year. Other taxpayers, especially those with non-payroll income, must make quarterly payments to the IRS. As long as these quarterly payments are made timely and the amount of the payments is sufficient in the eyes of the IRS you will not be subjected to underpayment penalties. However, if under paid, the IRS applies late payment penalties in addition to the income tax owed. This penalty applies even if you file your 1040 tax return on or before April 15th.

The Safe Harbor rule The tax code has a basic set of rules to determine if you owe a late tax payment penalty. The rule is call The Safe Harbor Rule. Here is a recap of the rule. If you follow the rules, you can avoid any penalties.

Late Payment Penalty Avoidance Tip If you are an employee there may be a way to avoid a penalty if you underpaid or neglected to pay your estimated tax payment for a quarter. Increase your payroll withholdings in later months of the year to build up your federal withholdings to cover the shortfall. Trying to catch up by paying more on your next estimated quarterly tax payment wouldn't work since the prior quarter's shortfall remains per IRS penalty calculations. For whatever reason, in calculating a potential underpayment penalty, payroll withholdings are treated as if they were all made at the beginning of the year, while quarterly tax payments (form 1040-ES) are tracked by the date received. To increase your withholdings simply provide your employer with a revised W-4. Just be careful that you leave enough in your paycheck to avoid other financial hardships. "Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA |

BLOGTo better serve our clients and friends, to keep you up-to-date and informed, our blog is a resource for tax tips and overall accounting related articles. We hope you find this useful! CATEGORIES

All

ARCHIVES

September 2023

|

RSS Feed

RSS Feed

|

Phone: (630) 320-3720

Monarch Accounting Group Inc 145 Tower Drive, Suite 10 Burr Ridge, IL 60527-7836 Email: Info@MonarchAccountingGroup.com |

|

|

|