New tax legislation eliminated the tax deferral on exchanges of like-kind exchanges of property, except for real estate. This change (generally effective in 2018) may apply to more transactions than you think. For instance, it comes into play when you trade in one business car for another.

Here's what matters for business vehicles Under prior law, no current tax was due on an exchange of like-kind properties, like vehicles, if certain requirements were met. You only had to pay tax on any "boot" you received (e.g., cash on a car trade-in). But now taxpayers must contend with a convoluted set of rules that could result in a taxable gain. Let's look at an example involving a trade-in before and after the new law:

There are other tax complications, but you get the basic idea. Keep these new rules in mind when you negotiate the price of a new business vehicle and the trade-in value of your old one. Alternatively, you might sell the vehicle personally and pay the full price for a new one. Call for help determining your best approach.

0 Comments

Last year’s Tax Cuts and Jobs Act made significant changes to the tax law that affect small businesses. The IRS posted two new resources on IRS.gov to help taxpayers understand how these changes affect their bottom line. Here are some details about these resources: New publication: Tax reform: What’s new for your business This electronic publication covers many of the TCJA provisions that are important for small and medium-sized businesses, their owners, and tax professionals to understand. This concise publication includes sections about:

New webpage: Tax Reform for Small Business This one-stop shop highlights important tax reform topics for small businesses. Users can link to several resources, which are grouped by topic:

More information: Tax Reform Small Business Initiative  After the new law repealed deductions for entertainment expenses, many business people figure their write-offs for treating customers or clients to meals are gone for good. But interim guidance handed down by the IRS provides some light at the end of the tunnel.

You may continue to deduct 50 percent of the cost of business meals if these conditions are met:

Here are three scenarios you may find yourself in and how the new business meals rules apply:

The IRS is expected to issue proposed regulations with more details soon. Until then, you can rely on the interim guidance. Call if you have questions about your business deductions.  Taxpayers can now get tax tips and helpful news from the IRS on Instagram. The agency just debuted it's official Instagram account, IRSNews, which users can access at www.instagram.com/irsnews or on their smartphone using the Instagram app.

Last year's tax reform law brought many tax law changes that will affect virtually every taxpayer. The IRS Instagram account will share taxpayer-friendly information to help people better understand these changes. The IRS will use its new Instagram account to:

The IRS will use Instagram along with several other social media tools to communicate with taxpayers:

The IRS also has their own app, IRS2Go. Taxpayers can use this free mobile app to check their refund status, pay taxes, find free tax help, watch IRS YouTube videos and get IRS Tax Tips by email. Like Instagram, the IRS2Go app is available from the Google Play Store for Android devices, or from the Apple App Store for Apple devices. IRS2Go is available in both English and Spanish. Qualified Opportunity Zones were created by the 2017 Tax Cuts and Jobs Act. These zones are designed to spur economic development and job creation in distressed communities throughout the country and U.S. possessions by providing tax benefits to investors who invest eligible capital into these communities. Taxpayers may defer tax on eligible capital gains by making an appropriate investment in a Qualified Opportunity Fund and meeting other requirements.

In the case of an eligible capital gain realized by a partnership, the rules allow either a partnership or its partners to elect deferral. Similar rules apply to other pass-through entities, such as S corporations and its shareholders, as well as estates and trusts and its beneficiaries. To qualify for deferral:

If a taxpayer holds its QOF investment at least five years, the taxpayer may exclude 10 percent of the original deferred gain. If a taxpayer holds its QOF investment for at least seven years, the taxpayer may exclude an additional five percent of the original deferred gain for a total exclusion of 15 percent of the original deferred gain. The original deferred gain – less the amount excluded due to the five and seven year holding periods – is recognized on the earlier of sale or exchange of the investment, or December 31, 2026. If the taxpayer holds the investment in the QOF for at least 10 years, the taxpayer may elect to increase its basis of the QOF investment equal to its fair market value on the date that the QOF investment is sold or exchanged. This may eliminate all or a substantial amount of gain due to appreciation on the QOF investment. More information:  New tax legislation provides numerous tax benefits for individuals for 2018 through 2025. But not all the changes are likely to align with your go-to tax strategy from previous years. Here are five big tax breaks that could leave you with a tax surprise come April 2019 if you haven't adjusted your current tax plan:

Small businesses should be on-guard against a growing wave of identity theft and W-2 scams. Employers hold sensitive tax data on their employees - such as Form W-2 data - which is highly valued by identity thieves.

All employers are targets for the W-2 scam. This scheme has become one of the more dangerous email scams. Here's how it works:

This scam is such a threat to taxpayers that a special IRS reporting process has been established. Here's an abbreviated list of how a business should report these schemes. They should:

The IRS urges everyone with any type of online account to review new, stronger standards to protect their passwords. Doing so will help protect against savvy cybercriminals who wants to access people’s accounts and steal their identities. Here are three steps people can follow to build a better password:

In addition to creating strong passwords, people can:

The IRS reminds holiday shoppers to protect their tax and financial data from identity thieves. All it takes is a few extra steps to prevent cybercriminals from stealing sensitive data, such as financial account information, Social Security numbers, and credit card information. Thieves could use this data to file a fraudulent tax return in 2019.

This tip is part of National Tax Security Awareness Week. The IRS is partnering with state tax agencies and its partners in the Security Summit to remind to taxpayers and tax professionals about the importance of protecting data. Cybercriminals want to turn stolen data into quick cash. They do this by draining financial accounts, charging credit cards, creating new credit accounts or even using stolen identities to file a fraudulent tax return for a refund. Here are seven steps taxpayers can follow to help protect their accounts and their money:

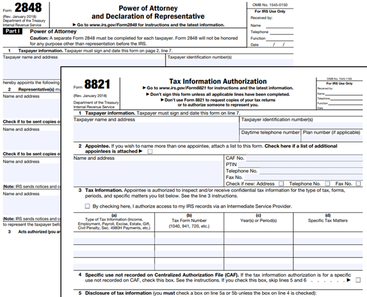

Did you know the IRS is prohibited from releasing information you report, except in limited circumstances? You have to grant specific authorization to allow someone to discuss your return with the IRS, receive copies of your returns or tax notices, or negotiate with the IRS on your behalf.

For example, say you receive an IRS notice, and you want your tax preparer to resolve the issue for you. The only way your preparer can help is if you have given permission allowing an exchange of information with the IRS. Here are three ways to grant authority for access to certain tax information:

The person you authorize will not automatically receive copies of IRS notices, but can review your information for the specific tax period. The authorization expires one year from the original due date of the return. Form 8821, Tax Information Authorization. This form is a disclosure authorization that allows the person you choose to automatically receive notices and other information about your taxes for periods you specify. You can revoke the authorization by submitting a signed copy of the original with the word "Revoke" written across the top. Form 2848, Power of Attorney and Declaration of Representative. The power of attorney lets someone who is eligible to practice before the IRS represent you and, in some cases, sign agreements and other documents on your behalf. You can revoke a power of attorney by filing a new one for the same tax period, or by sending a signed copy of the original with the word "Revoke" written across the top. Other forms may be required, depending on the type of tax information and how much authority you want to grant. Give us a call for help granting authorization. |

BLOGTo better serve our clients and friends, to keep you up-to-date and informed, our blog is a resource for tax tips and overall accounting related articles. We hope you find this useful! CATEGORIES

All

ARCHIVES

September 2023

|

RSS Feed

RSS Feed

|

Phone: (630) 320-3720

Monarch Accounting Group Inc 145 Tower Drive, Suite 10 Burr Ridge, IL 60527-7836 Email: [email protected] |

|

|

|