Especially parents, grandparents and relatives For parents, challenges come from every direction – feeding times, car seats, sleep schedules, strollers, child care and of course ... taxes. What most parents do not consider is that these bundles of joy complicate their tax situation!

Whether you are a parent, grandparent, or know someone who is expecting, here are some tax tips to consider:

"Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA

0 Comments

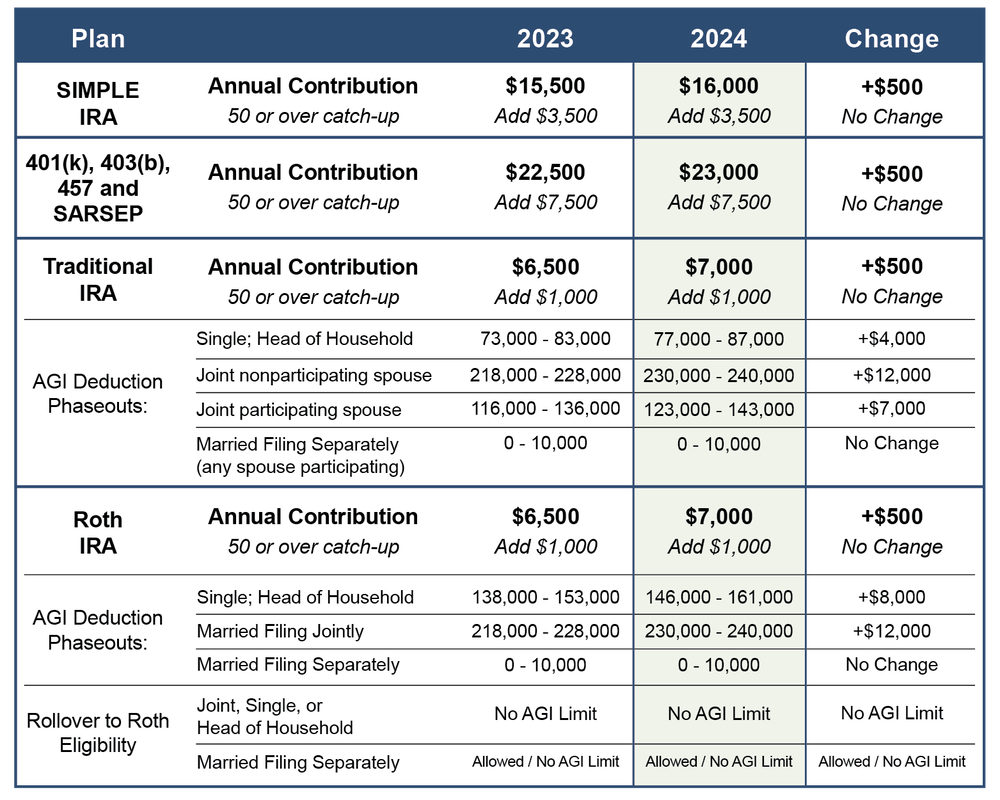

As part of your planning for next year, now is the time to review funding your retirement accounts in 2024. Recent cost of living calculations means much higher contribution limits for next year. Plus the higher income phaseouts for eligibility will make many more taxpayers eligible for fully-deductible contributions. So plan now to take full advantage of this tax benefit. Here are annual contribution limits for the more popular programs:  How to use

Other ideas If you have not already done so, also consider:

"Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA You will be surprised how many are impacted In the fourth move in three years, the IRS in late November changed the reporting requirements for Form 1099-K. So why should you care? Well pay attention if you’ve ever sold anything on Amazon or eBay, have ever sold tickets to sporting events or concerts, or received money from payment apps like Venmo.

Background The IRS wants to track the receipt of money from third-party credit card and other payment processors. This is because much of this activity is deemed business activity AND it is under-reported. The IRS uses Form 1099-K to report these transactions and for years the threshold for reporting was $20,000 and 200 transactions per payment processor. The law was then changed to lower the threshold to $600 and any number of transactions. Current situation After delaying the implementation of the $600 threshold two times in prior years, the IRS once again rolled back the reporting threshold for 2023 to $20,000 and 200 transactions. This repeated change, albeit a welcome one for many taxpayers, is also creating mass confusion as the delay was put in place a mere 45 days before the forms start hitting inboxes. What you need to know The income is reportable whether you receive the form or not. So if you have a side hustle on Amazon, or have a business reselling tickets, you are required to report it. You may OR may not receive a Form 1099-K. Given the late change, you may still receive a Form 1099-K this January or February even if the payment processor is not required to report it. So if you receive a form, please keep it. The activity is still being reported to the IRS. The limits are still coming down, so be prepared. The recent change is only temporary. The IRS will be lowering the threshold over the next few years to get to the $600 limit, so be forewarned. How to report business activity varies. If you have a side hustle, sell or resell tickets online, or use digital payment systems to receive payment for goods or services you are in business. This needs to be reported. How it is reported can vary so call for help. "Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA When to know to conduct a tax review Here are some tips that should trigger you to conduct a full tax planning session to ensure your tax bill next year is not higher than it needs to be.

1. You owed tax last year. If you have not adjusted your withholdings, you could be in for a big tax bill. Time to take a look and plan accordingly. 2. Your household income changes dramatically. Whether higher OR lower, a change in income will impact your taxes, especially if it impacts availability of deductions or credits. 3. You are getting married or divorced. Married filing joint brings benefits and tax surprises. So does the impact of being single once again. 4. You have kids attending college next year. There are a number of tax programs that can help. 5. You have a small business. There are depreciation benefits plus the qualified business income deduction to consider. Plus you will need to understand the flow through impact your business profits will have on your personal tax return. 6. You plan on selling investments. Capital Gains tax rates can now range from 0% to 37% (depending on long or short term gains and your income level). 7. There are changes in your employer provided benefits. These changes could impact your taxable income this year. 8. You buy, sell or go through home foreclosure. There are tax benefits AND tax surprises when you buy or sell a home. A planful approach can make all the difference. 9. You have major medical expenses. The threshold for itemizing medical deductions is 7.5%. This means to itemize these expenses, they must exceed 7.5% of your income. But with proper planning, there are other ways to pay these expenses with pre-tax money! 10. You recently lost or changed jobs. Federal unemployment benefits are taxable and need to be accounted for in your tax plan. 11. Your estate has not been reviewed in the past 12 months. New gift tax and estate tax laws make 2023 a key year for an estate tax review. 12. You have a new child or dependent. These treasures bring joy AND a different tax obligation! If any of these triggers apply to you, please schedule a tax planning appointment. "Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA  Selling property to a family member or loved one is deemed a related party transaction by the IRS. If contemplating a transaction like this, you need to review the tax consequences of your decision BEFORE you act. As you might imagine, related party transactions covers relatives like your children, grandchildren and siblings, but it also applies to business entities you own. Here are four common situations you may encounter, and tips to help you avoid tax trouble:

1. Installment sales. When selling your property over two or more years, your transaction is deemed an installment sale. With an installment sale you can defer tax on your gain until the tax years in which payments are actually received. However, if you sell the property to a related party who disposes of it within two years, the remaining tax is due immediately! Tip: To solve this problem, insert language in the legal agreement with your related party that does not allow the disposition of the property within two years. 2. Selling at a discount. If you’re selling a house to a related party, you may wish to give that person a sweetheart deal. Unfortunately, the IRS may reclassify the transaction as a gift if the property is sold at considerably less than its fair market value (FMV). Fortunately, you have some wiggle room. If you discount the sale by less than 25 percent, you should be OK. Tip: Err on the side of safety by having an appraisal of the property before the transfer date OR build documentation that justifies the FMV. 3. Transferring remainder interests. In some cases, a homeowner may transfer an interest in a home to his or her estate while continuing to live there. Although this may meet certain objectives, the estate can’t take advantage of the $250,000 home sale exclusion ($500,000 for joint filers). However, if the heirs subsequently meet the two-out-of-five-year ownership and use requirements, the exclusion becomes available. Tip: Prior to transferring interest in your home to anyone (including a trust or an estate), understand the impact of this action on the tax-free home gain exclusion. 4. Like-kind exchanges. Often, instead of selling business or investment property, an owner may trade for another, similar property hoping to either defer or avoid taxable gains. Under recent legislation, tax-free exchanges of like-kind properties are eliminated, except for qualified real estate transactions. Tax is generally deferred until the replacement property is sold, but the tax law imposes a two-year holding requirement on the parties to the deal. Alternatively, you may qualify under a special exception, such as proving tax avoidance wasn’t the purpose of the sale. Tip: Related property transactions of this type can get complicated. Ask for a review of your situation before trading any property. Transferring assets, including property, to family gets the attention of the IRS. Should you be contemplating this, reach out for assistance before making the move. "Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA  Too often taxpayers receive tax surprises at year-end due to actions taken by mutual funds they own. What can add insult to injury is the unsuspecting taxpayer who recently purchases the shares in a mutual fund only to be taxed on their recent investment. How does this happen and what can you do about it?

Tax surprises Towards the end of each year, many mutual funds pay a dividend to the holders on record as of a set date. The fund might also distribute funds deemed as capital gains based upon buying and selling activity that takes place in the fund throughout the year. This can create many problems:

Here are some ideas to help reduce this mutual fund tax surprise:

"Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA Your best audit defense The IRS is being very public about increasing the review of tax returns. The best defense for you is to be prepared before it happens. Here are some suggestions:

The one-two punch To prove your deduction, most auditors look for two key documents: receipts and proof of payment. 1. Receipts. This is the first of the key documents you must have to validate a deduction. The receipt should clearly show the company or entity, the date, the value of the activity and a clear description of the activity. In the case of donations, the receipt should also have a statement that confirms you received no benefit in return for your donation. It should also state that you are not retaining part ownership of the donation. 2. Proof of payment. The second key document to defend your deduction is proof of payment. You will need a canceled check, a bank statement or a credit card receipt and related statement. Contemporaneous is key Your proof of payment and receipts should generally match the date of the activity. The IRS is quick to dismiss receipts that are obtained after the fact. A good rule of thumb is to ensure receipts and proof of payment are received at the time of the activity. If not, at least make sure you have receipts and payment proof within the tax year the deduction is taken. Other proof is often required In addition to the above, there are certain deductions that require additional documentation. Here are the most common; Mileage logs. You will need to show properly-maintained mileage logs for business miles, charitable miles and any medical mile deductions. Business records. You will need financial statements for any business-related activity with supporting documentation. Residency. If you live in multiple states or multiple countries, you may have to prove where you lived during the year. In addition, to receive the capital gain exclusion for a home sale, you will need to prove residency for two of the last five years. So keep records that show your physical presence to support your tax filings. Non-reimbursement. If you claim any education credits, you will need to show that you actually spent money for qualified expenses at qualified institutions. You will also need to show that your claimed expenses were not reimbursed through scholarships or grants. Defending your tax return during an audit can seem daunting. Fortunately, with some thoughtful planning, an audit can readily turn into a NO CHANGE audit. "Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA  Everybody likes getting something for free, and taxes are no different. If you invest in securities such as municipal bonds (munis) or municipal bond funds, you can generate tax-free interest income. Here is what you need to know.

Advantages of municipal bonds You pay zero federal tax on municipal bond investment income. This makes municipal bonds more attractive than many comparable taxable investments. A municipal bond paying 6 percent to an investor in the 24 percent tax bracket is actually a better investment than a taxable bond paying interest at 7.9 percent, due to the federal income tax break. What’s more, municipal bond income isn’t counted for net investment income tax purposes. So if you are subject to this 3.8 percent surtax, municipal bonds provide an additional tax break to you. And, if the bond is issued by an authority within the state where you reside, it’s also exempt from any state income tax. For these reasons, municipal bonds are a popular investment, especially among retirees because they are often stable, and most bonds carry a relatively low risk. Potential consequences While the benefits of municipal bonds make it an attractive option for many investors, there are potential downsides:

Investing in municipal bonds can provide tax-free, stable income, but you need to understand how the investments fit with your situation to maximize the tax savings. "Tax Tips" are published to provide current tax information, tax-cutting suggestions, and tax reminders. If you would like more information on anything in "Tax Tips," or if you'd like to be on our mailing list to receive other tax information from time to time, please contact our office. The tax information contained in this site is of a general nature and should not be acted upon in your specific situation without further details and/or professional assistance. We are trusted CPA advisors servicing Burr Ridge, Hinsdale, Willowbrook, Darien, Naperville, and all Chicagoland area. Do you need assistance with your business and/or personal tax returns? Would you like to have a trusted source for your accounting, allowing you additional time to focus on increasing your business? Do you use QuickBooks, or plan to in the future, for your accounting? We include these in all our service packages, customized to fit your personal or business needs. We are currently accepting new clients. Your initial consultation is free, so you have nothing to lose and everything to gain. Our experienced staff is available to help you streamline your accounting, giving you more free time for yourself. Set up an appointment today by calling (630) 320-3720 or email us at info@monarchaccountinggroup.com. For more free resources, such as Tax Organizers, and Record Retention Schedules, access our website www.monarchaccountinggroup.com. Mia Verc, CPA; Janice Papais, CPA WASHINGTON — The Internal Revenue Service announced today that the amount individuals can contribute to their 401(k) plans in 2024 has increased to $23,000, up from $22,500 for 2023.

|

BLOGTo better serve our clients and friends, to keep you up-to-date and informed, our blog is a resource for tax tips and overall accounting related articles. We hope you find this useful! CATEGORIES

All

ARCHIVES

September 2023

|

RSS Feed

RSS Feed

|

Phone: (630) 320-3720

Monarch Accounting Group Inc 145 Tower Drive, Suite 10 Burr Ridge, IL 60527-7836 Email: Info@MonarchAccountingGroup.com |

|

|

|